The year 2013 is going to be remembered for a myriad of reasons. Some investors and speculators may have already sent a “Thank you!” note to the bearded man who made possible the amazing profits experienced by those who decided to buy the S&P 500 at an early stage. However, those who invested in Emerging Markets and precious metals might have had a tough time throughout the year.

|  |

Although each one resembles the other, if you have Santa Claus in mind, I'll be sorry to disappoint you. The catalysts were Ben Bernanke and his famous unconventional monetary policy decisions.

The driving factors last year were QE and the "taper tantrum."

Since May every single trader had been trying to predict when and by how much the Fed would reduce its asset purchases, until the move was finally made.

"Tapering is not tightening"

This move is welcomed by critics of QE who fear the Fed is fuelling price-bubbles and storing up trouble for the future. Nevertheless, withdrawing the artificial stimulus will act as a drag on growth, whether tightening or not. Personally, I don't trust Fed's maxim "our poison is our solution: debt." However, is there any other solution at all? At this moment in time I don't know. As traders, we just have to adapt and make profits from it; as a society though, here's a precious opportunity to learn from.

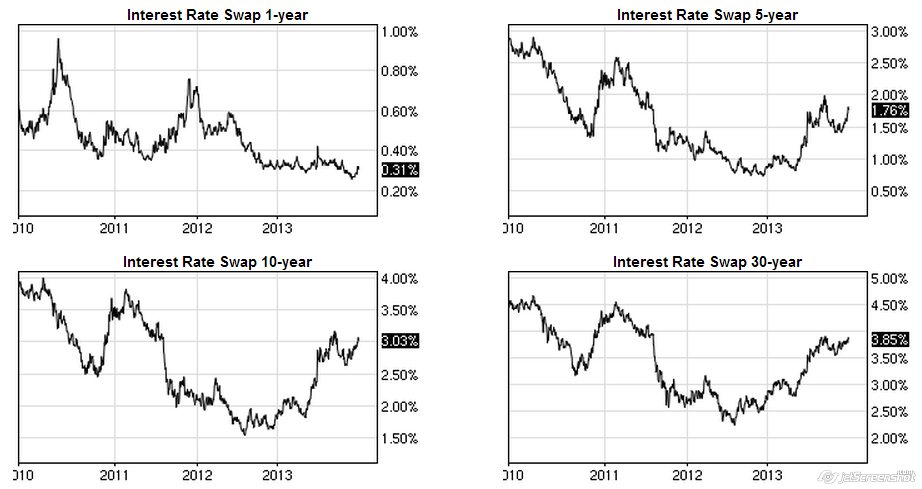

When the tapering scheme was first disclosed, it provoked an intense and immediate reaction on yields and interest rate swaps.

Poor bond investors.

A lot of people now foresee what could be a monetary transition from bonds to stock markets. However, due to the high price of some stock exchanges and an already diminishing monetary stimulus, this transition is not likely to be frenzied (if any).

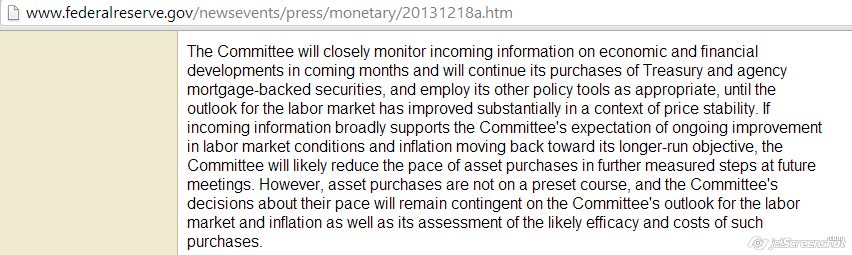

In December, the Fed decided to scale back its $85bn of monthly asset purchases by $10bn effective in January 2014. Even though this "tapering" decision had been long awaited, it was relatively small. "Foward guidance" is also helping to assuage some of the instant reactions that the end of QE infinity is likely to bring: The Fed has promised to maintain interest rates at present levels "well past the time unemployment declines below 6.5 percent." Moreover, the Fed also said the following in the 2013 December FOMC statement:

In summary, they're clarifying that if the Comitee's outlook turns negative or not as possitive as expected, they can always increase their monthly asset purchases or postpone any reduction. This is what forward guidance is all about: exploring new horizons.

What does Janet Yellen think about this?

| “Now, this is challenging: We’re in unprecedented circumstances, we’re using policies that have never really been tried before -- and multiple policies -- and we’re trying to explain to the public how we intend to conduct these policies. So, it is a work in progress, and sometimes miscommunication is possible." - Janet Yellen |

I think the main driving factors in 2014 will continue to be the Fed and it's policy decisions. If the US continues to grow at the current pace, the Fed's pledges to keep interest rates at present levels might be at peril. Upward revisions in growth forecasts have already been announced by the IMF. So, maybe keeping interest rates this low too long won't be possible.

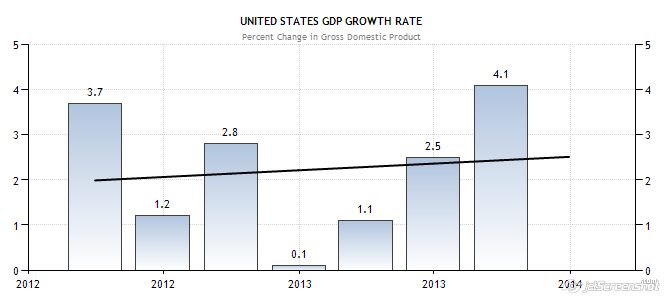

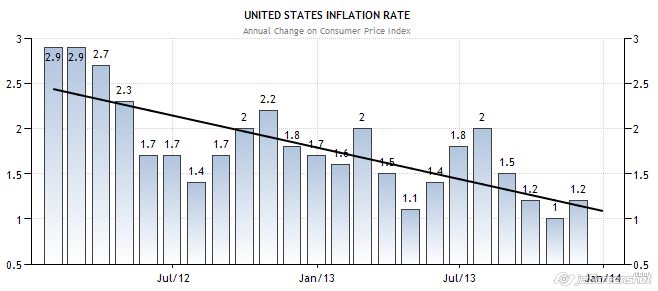

Let's check the US numbers for the year 2013.

Overall, everything but inflation looks great. Ben Bernanke launched QE with the goal of avoiding deflation, thus this bearish inflation rate is not as catastrophic as some people may suggest or as it could have been.

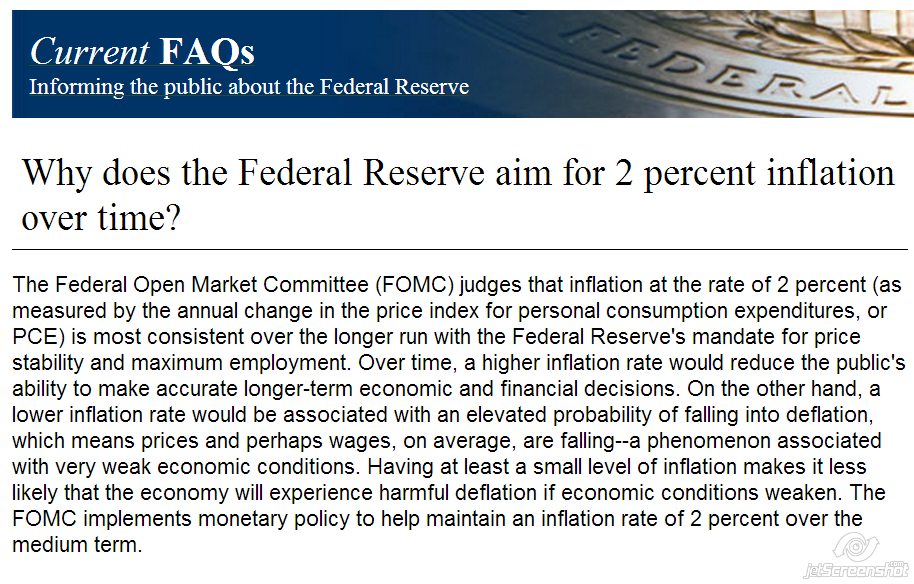

However, it's still a bit far from achieving the 2 percent inflation target.

There were other fraught situations though...

Thank god it's over now.

The political acrimonious state of affairs in the US (remember the government shutdown?) has been defused by the two-year budget agreement that virtually ensures there’s not going to be any (we’ll see) difficulty alluding them.

It makes me a bit furious to know that these political clashes between Republicans and Democrats had taken at least 0.6 percent off the GDP.

Going back to the equity markets, because a lot has been said about the S&P 500 being overvalued, I decided to investigate about correlations between the Federal Reserve's balance sheet and the S&P 500; I found this video:

Since the banks excess reserves subject made my curiosity spark, I continued reading and found this New York Fed paper explaining in a taxpayer-friendly way why banks are holding so many reserves:

Let's go further...

I recommend you to skip the whole marketing and start watching this video from minute 7:40

What's going to happen this year?

We'll find out together.

Happy 2014!

RSS Feed

RSS Feed