"Borrow New and Repay Old" or "Deleveraging"

|   |

After many years of managing an economy fundamentally driven by credit-fuelled investment, exports, construction of infrastructure and real estate, China's authorities have decided to transform their investment-propelled economy into a consumption-driven one, as well as to start deleveraging banks in order to avoid a credit crisis that could substantially imperil their economic and financial future.

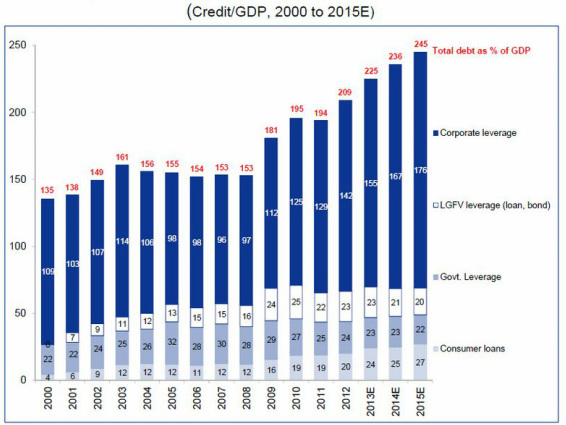

Although anyone who comes across this website and has a quick glance at the debt chart below could instantaneously conclude that the PBoC doesn’t have a clue about risk management, he or she would be wrong.

And if that person believes in what I said just because it’s on the internet, then he or she would be doubly wrong.

| So, what’s happening in the People’s Republic of China? |  |

Keep reading and you’ll find out ;)

In December 2013, an official audit showed that local government debt levels increased 70% to almost $3tn in less than three years. Around 60% of that total amount will mature before the end of 2015. If you think that's far away, let me tell you that 40% of those $3tn will mature before this year comes to an end.

Nevertheless, according to an audit in 2010, more than 50% of local government debt should had matured before the end of 2013.

Mmm... what's happening here?

Chances are that the debt wasn't paid back, but refinanced.

At the end of 2013, the National Development and Reform Commission (NDRC) announced that China had given local Governments permission to issue bonds as a way of rolling over their debt.

|  |

“If construction projects face funding shortfalls and there is no way of completing the project to realize expected revenues, we will consider granting permission for these platform companies to issue an appropriate amount of new debt.”

|   |

Many of the original loans were used to finance construction and infrastructure projects that normally take a lot of time to provide revenues. Since rollovers are seen as one of the few viable options to avoid default in these cases, it’s no surprise getting deeper in debt has been the preferred choice.

“The funding that is raised can be used to ‘borrow new and repay old’ and for incomplete projects, ensuring that they will not end up half-finished.”

The NDRC also recommended refinancing debt via bonds instead of loans because they could be issued at lower rates and for longer maturities, plus they would spread risks from banks to the capital market.

Whether it’s via bonds or high-interest loans, the need for rollover points out the complex debt situation that China is facing as it struggles to deleverage banks without unleashing an outright Day of Reckoning.

What is China doing to address this problem?

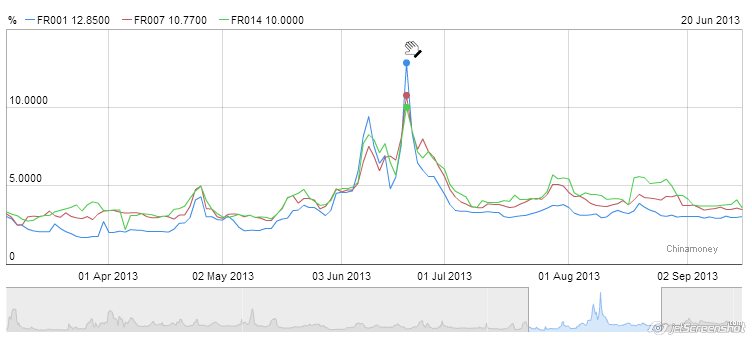

The PBoC is attempting to deleverage banks by spreading a “little” fear in the money markets. It has been guiding interest rates higher so banks finally understand that they should not rely on short-term liabilities in the interbank market to finance risky long-term assets like loans to property companies and local governments.

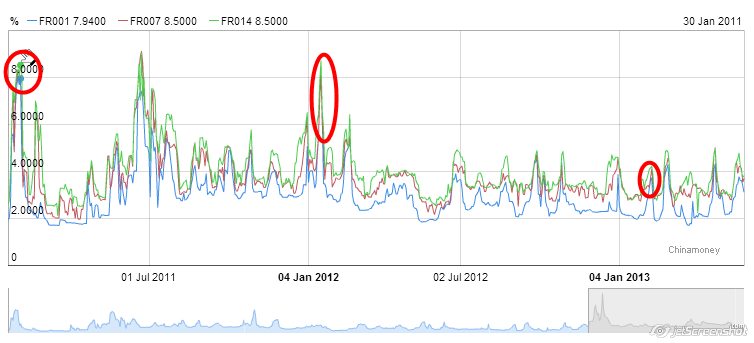

Even though letting money markets rates breach the 10% level may not had been in the PBoC's scheme, that's exactly what happened during the June Credit Crunch.

Normally, when banks don't have enough money to satisfy regulatory requirements and to meet their obligations to customers and creditors, the PBoC steps in and injects enough liquidity so they're able to continue carrying out their daily operations as usual. However, when that happened in June 2013, the PBoC stubbornly refused to lend any money, hence causing the credit crunch.

| Many analysts believe the PBoC miscalculated the reaction. |

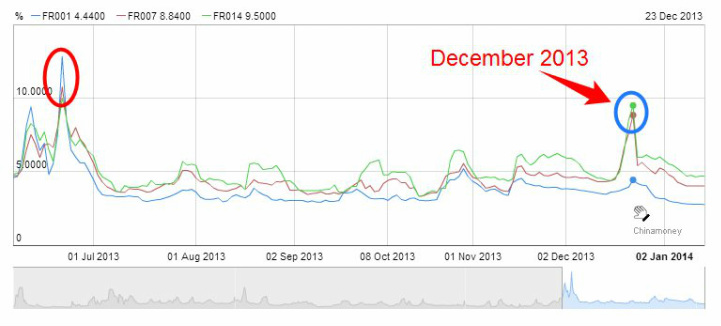

Something similar happened in December

Banks were reluctant to lend each other in December. Likewise, the PBoC refused to assuage the cash-strapped banks' thirst for money through its regular open-market operations; instead, it allowed money markets rates to go higher at a time when banks faced regulatory pressure to book more deposits as the year came to an end.

| I'd say it was a warning for 2014 In order to prevent a disaster, the PBoC decided to provide an emergency dose of credit via "short-term liquidity operations" (SLOs). |

"The medicine, seemingly, has worked"

I think the PBoC is likely to continue sitting on its hands from time to time as a way of spreading the caveat that banks should improve their liquidity management. Otherwise, there could be stern consequences.

What could happen now?

Seasonally, as the Chinese New Year comes, banks need to prepare themselves with additional money for cash withdrawal and holiday consumption payment. As a result, cash demand usually rises sharply and interbank liquidity becomes tight, thus money markets rates rise.

Who knows? Perhaps the PBoC will play a decisive role in intensifying the seasonal spike this month.

Personally, I think China will strengthen its statements by basing them on facts this year. I think they won't be lenient or merciful anymore.

Even if China doesn't have to abide another cash crunch such as the one we saw back in June, 2014 will be a harsh year for its money markets without doubt.

Check out this report about China's reforms frailties

Compare them with what has been already done ;)

China wants to do things right. How well it actually does will depend a lot on its politicians. My bet is that the economic decline will continue to be gradual in 2014. If there's any wrong move made by the Chinese authorities, an enormous economic decline could become indisputable.

I wouldn't want that to happen

RSS Feed

RSS Feed